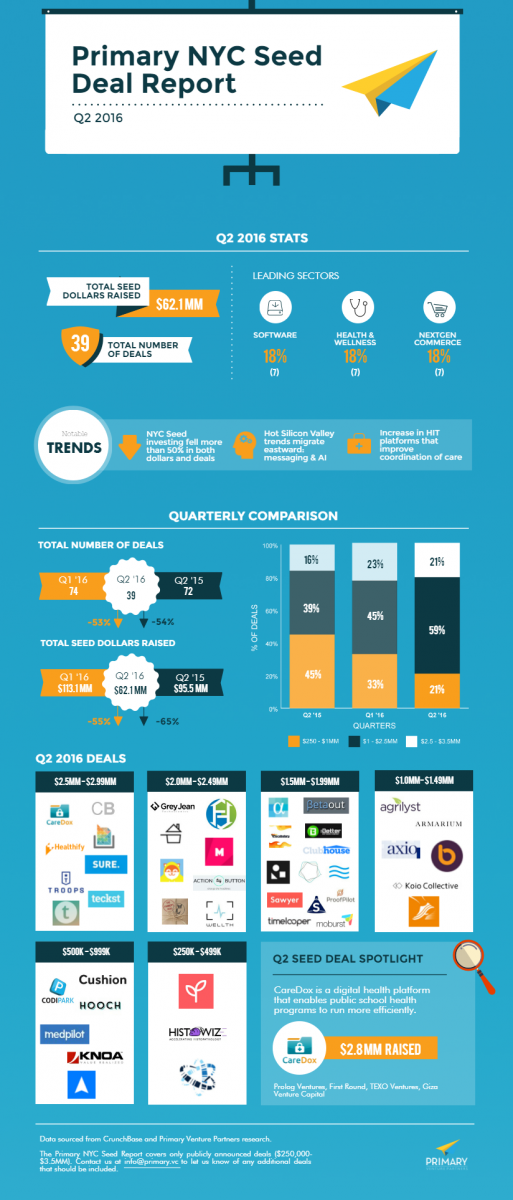

The honeymoon may finally be over. The 'everything is shiny and new,' with a healthy dose of adrenaline phase has come to an end, and it’s time to hunker down for some good, old-fashioned business-building. The big news from Q2? After 2015’s near record breaking VC funding and sky-high valuations, seed investing in NYC dropped more than 40 percent for Q2, on both a dollars and deals basis.

We began comprehensively tracking the activity in the NYC seed community last quarter, with the release of our first NYC Seed Deal Report. With this second edition, we’ve witnessed a marked slowdown in activity, suggesting that — despite NYC’s relative hot streak — our market isn’t immune to the cooling effect the startup ecosystem is experiencing on a national scale.

NYC Seed Deal Trends: Q2 2016

NYC Seed Deal Trends: Q2 2016

All in all, Q2 was a strong one for enterprise software, with a bit of a slow-down on the NextGen Commerce front. Here are some notable trends that emerged from the Seed deals that closed this quarter:

Two of Silicon Valley’s hottest areas for investing —messaging and artificial intelligence — are migrating East. Q2 saw local fundings for advanced communication and messaging platforms (Teckst, Bontact) as more enterprises realize the value of messaging platforms to communicate internally and with their customers. And on the AI front, Clarity Money, which claims to be your personal “money guru”, and Troops, a Slack bot for sales teams, may be some early glimmers of NYC developing its own AI ecosystem.

Q2 saw an uptick in healthcare-related investments touching on various parts of the healthcare ecosystem, with particular attention on startups that improve coordination of care for various populations. CareDox enables public school health programs to run more efficiently, while Healthify improves access to social services for low-income communities. Other healthcare-related deals in Q2 centered on companies that simplify a complex and often archaic industry: MedPilot brings efficiency to medical billing and collections departments; ProofPilot simplifies the process of conducting scientifically valid research studies; and Wellth offers financial incentive programs to improve patient adoption and adherence rates.

Q2 shows continued growth in the areas of subscription services (Skyfit offers on-demand access to studio-quality fitness classes; Sawyer provides subscription-based access to neighborhood kids’ classes) and the sharing economy, with deals announced for Armarium, an on-demand luxury styling service, and Homemade, a platform that allows cooks to market and sell their food. And while there’s a general feeling in the market that the sharing economy is here to stay, questions have started to emerge about the oversaturation of the subscription space.

The quarter also saw growth in the number of startups calling Brooklyn home. 14 percent of Q2 deals came out of the borough, up from just three percent last quarter, and 10 percent at this time last year. It’s no secret that Brooklyn has been rising in prestige in the tech startup world, having hosted TechCrunch’s Disrupt NY for the first time in May, and with Sunset Park’s Industry City earning itself a good bit of media buzz. As the rise of Manhattan real estate rates continues unabated, we can expect to hear more noise out of Brooklyn in the coming quarters.

Click here for the full breakdown of Q2’s completed Seed deals, including company overviews, funding amounts and investors.

Cloudy, with a chance of cautious optimism

Following a near-record-breaking year of VC spending, founders and investors put the brakes on in Q2 2016. NYC saw just 42 Seed deals in the quarter, totaling $66.7 million in funding. These figures are down 43 percent and 41 percent, respectively, from Q1 2016, and 42 percent and 30 percentdown, respectively, from this quarter last year.

These downward trends have caused investors (and companies alike — see WeWork’s recent decision to slim down, among many other recent fat cutting stories) to put more emphasis on monitoring cash flow, valuations to return to more palatable proportions, and the speed around Seed deals to decelerate. With later-stage financings dwindling on a national level, Seed investors are spending more time helping their existing companies raise new money, while at the same time working feverishly to rationalize spending and trim burn rates. So we’re left with the double-whammy of increased time spent working with existing portfolios, and a general sense of unease at the thought of adding more companies to a market that’s already too large for the collective appetite of the Series A investor universe. The result? Fewer seeds planted.

Larger funding rounds lay the groundwork for long-term success

For the deals that are getting done, we see a continued trend toward larger rounds. This may be driven by a desire to increase the likelihood of Series A success; by providing more initial runway, companies will have more time to clear the increasingly high bar of Series A investors. Put simply, more Seed capital is a hedge against uncertainty in the funding environment down the road.

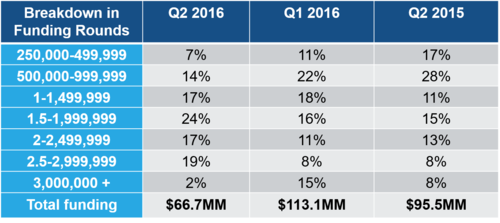

In Q2, 60 percent of seed deals were in the $1.5—$3 million range, up from 35 percent last quarter and 36 percent in Q2 2015. The most well-funded bucket this quarter — with 24 percent of deals — was the $1.5—$2 million range (compared to 16 percent last quarter, and 15 percent in Q2 2015), and we see an even bigger increase in the $2.5—$3 million bucket, with more than double the number of deals falling into that range this quarter compared to both Q1 2016 and Q2 2015. At $1.6 million, average deal size this quarter is up over 20 percent from a year ago.

Macroeconomic forces threaten an already-tenuous foundation

An unfortunate blend of macroeconomic factors is adding to the overall feeling of discomfort in the market right now. And while Seed investors boast of being less directly impacted by the public markets and broader economy, a tidal wave of political upheaval certainly won’t bolster investor confidence. Increased global terrorism, Brexit and, of course, our current election telenovela all add to the uncertainty. Election years, particularly those coming off of an eight-year presidential term, have been known to cause consistent public market tumult.

On the flip side, the tech IPO market showed some signs of life in Q2, with the public offerings of SecureWorks, Acacia Communications, NantHealth and, of course, Twilio — the first unicorn company to go public since Square last November. Needless to say, people are keeping a watchful eye on Twilio’s stock, in hopes that its success will signal a genuine reopening of the IPO window.

Looking ahead to Q3

As we continue to ride out the storm of uncertainty, we expect to see similar deal flow on both the NextGen Commerce and SaaS ends of the market in Q3. Tinged with the familiar, coconutty scent of summer, the NextGen Commerce universe may see ongoing sluggishness, with continued growth in the healthcare and fintech arenas picking up some of the slack. Or perhaps Q3 may fare better than expected, rebounding on the heels of some tech IPO successes? As macroeconomic forces continue along their precarious course, we’ll be keeping a close eye on the NYC Seed market for signs of change.

*It should be noted that the Primary NYC Seed Deal Report covers only those seed deals — which we define as $250,000—$3,500,000 — that have become public. We know there are deals that have closed but not yet been announced, including some of our own, and those will be added in once they are public.

Have a news tip for us or know of a company that deserves coverage? Let us know or tweet us @builtinnewyork.